Mold Insurance & Finance Guide 2026

Does insurance cover mold? The answer depends on the “Sudden vs. Gradual” rule. Plus, how to deduct remediation from your taxes using IRS Pub 502.

Trusted Sources: This financial guide references policy standards from the Insurance Information Institute (III) and tax codes from the Internal Revenue Service (IRS).

Mold remediation is expensive, often costing between $2,000 and $10,000. Homeowners assume their insurance will cover it, only to receive a denial letter stating “Gradual Damage Exclusion.”

Understanding the financial side of mold—from insurance loopholes to tax breaks—can save you thousands of dollars in 2026.

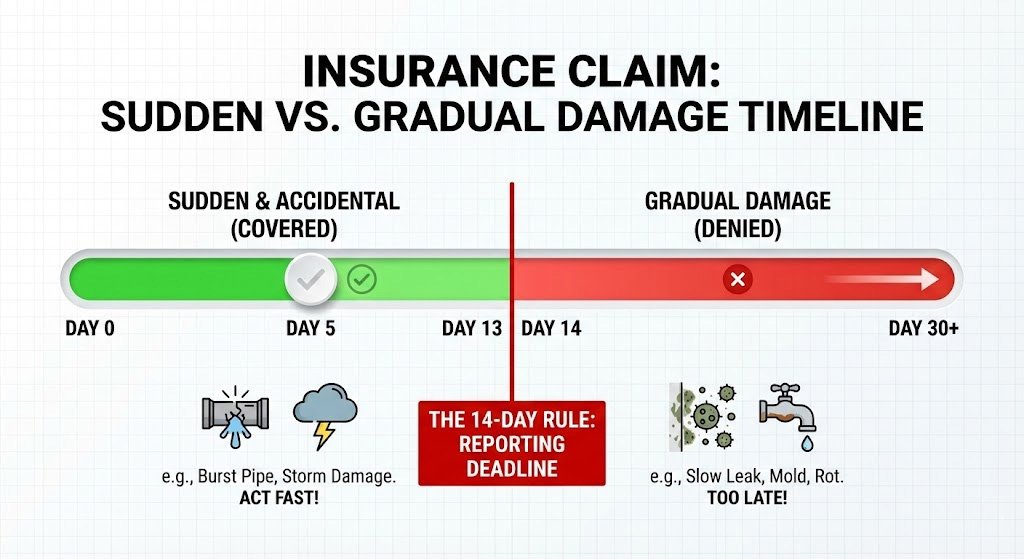

1. The “Sudden & Accidental” Rule

This is the single most important concept in mold insurance. Standard HO-3 policies do not cover “maintenance issues.” They only cover accidents.

Covered (Sudden): A pipe bursts while you are at work. You find it immediately and file a claim.

Denied (Gradual): A pipe has a pinhole leak behind the wall for 6 months. You didn’t know, but the insurance company considers this “neglect” because it happened slowly over time.

| Scenario | Insurance Outcome | Why? |

|---|---|---|

| Burst Pipe | Approved | Sudden event. |

| Leaking Roof (Old) | Denied | Considered “Wear & Tear.” |

| Flood (Weather) | Denied | Requires separate Flood Insurance. |

| Sump Pump Failure | Maybe | Only if you have “Water Backup” endorsement. |

“Never use the word ‘mold’ when you first call your insurer. The moment you say ‘mold,’ the agent checks your policy for a Mold Exclusion cap (usually $5,000). Instead, report the ‘Water Damage’ (the burst pipe). The water damage coverage limits are often much higher, and the mold removal is simply part of drying out that water.”

2. 2026 Remediation Cost Averages

According to the latest 2026 industry data, remediation costs range from $15 to $30 per square foot. However, costs vary wildly by location.

- Attic Remediation: $1,500 – $5,000 (Requires ice blasting).

- Crawl Space: $3,000 – $8,000 (Often involves encapsulation).

- HVAC System: $2,000 – $10,000 (If ductwork needs replacement).

3. IRS Tax Deductions (Medical Expense)

Can you write off mold removal? Yes, but only under strict conditions outlined in IRS Publication 502.

It falls under “Capital Expenses” for medical care. You must prove the remediation was medically necessary (Doctor’s Note) for a specific condition like asthma.

(Cost of Remediation) − (Increase in Property Value) = Deductible Amount

Example: You spend $10,000 removing mold. The appraiser says your home value did NOT increase because you were just restoring it to baseline.

Result: You can deduct the full $10,000 (subject to the 7.5% AGI threshold).

4. FHA & VA Loan Requirements

Government-backed loans have stricter standards than conventional loans.

- FHA Loans: Appraisers look for “Safety, Security, and Soundness.” Visible mold is a “health hazard” and must be remediated before closing.

- VA Loans: Require a “Section 1” pest inspection. “Fungus and Dry Rot” are classified alongside termites. The VA will not fund a loan until the property is certified clear.

5. Deep Dive Resources

Select a specific topic below for detailed financial strategies.

Detailed breakdown of costs per square foot for attics, basements, and ducts.

How to fight a “Gradual Damage” denial from your insurance adjuster.

How to use the IRS Capital Expense Worksheet to write off remediation.

Will mold kill your deal? Appraiser checklists for government mortgages.